Skip to content

Skip to content

You visit the doctor. You have two health insurance plans. Both should help pay the bill. But which one pays first? How much does each one cover? And can you end up with zero out-of-pocket costs?

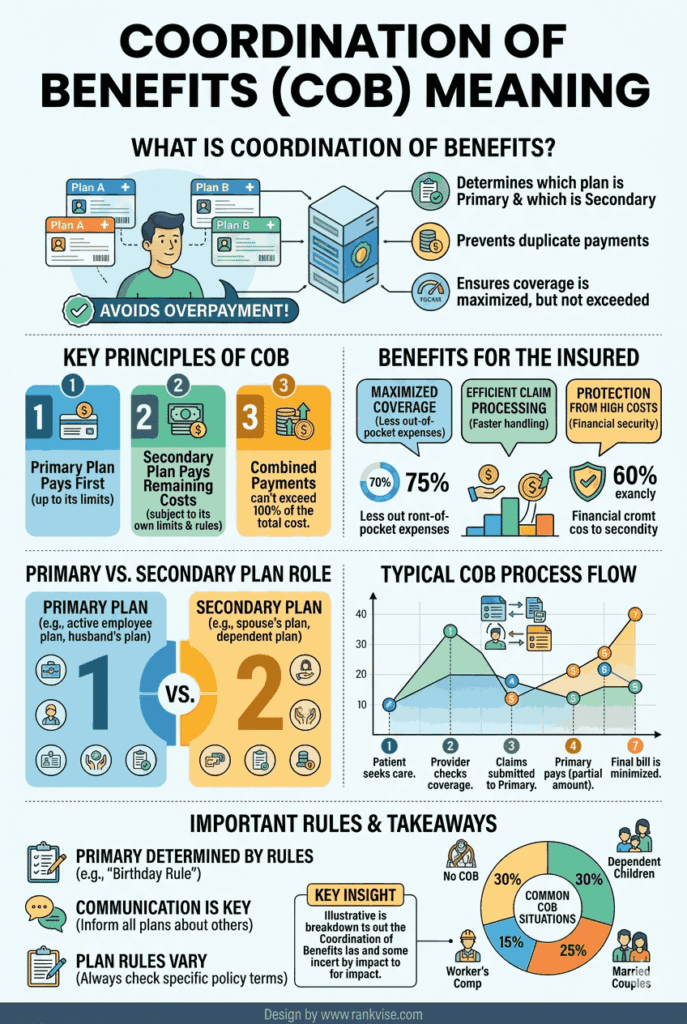

- Coordination of benefits is insurers' process to allocate payments so medical expenses are covered without duplicate payments or overpayment.

- Primary plan pays first; secondary pays remaining eligible balance using rules like subscriber, birthday, active employment, and longest coverage tiebreaker.

- Dual coverage can lower out-of-pocket costs but not exceed 100% of charges; always inform both insurers and compare premium costs.

These questions are exactly what coordination of benefits answers. It is one of the most misunderstood concepts in health insurance. Yet it affects millions of people who carry coverage under more than one plan.

This guide explains the coordination of benefits meaning in plain language. You will learn how insurers decide which plan pays first, what rules they follow, and how the process impacts your medical bills in real-world situations.

What Does Coordination of Benefits Mean?

Coordination of benefits is the process health insurance companies use to divide payment responsibilities when a person has coverage under two or more plans. The goal is straightforward — make sure your medical expenses get paid without overpaying beyond the actual cost of care.

Insurance companies often abbreviate this as COB. Every major insurer and government programme, including Medicare, follows coordination of benefits rules. These rules prevent duplicate payments and determine the order in which each plan processes your claims.

Without coordination of benefits, two insurers might each pay the full amount for the same medical service. That would result in the healthcare provider or the patient receiving more than the actual cost of treatment. COB rules exist to prevent that overpayment while still maximising the coverage available to you.

In simple terms, coordination of benefits is the system that decides who pays what when you have dual insurance coverage.

How Does Coordination of Benefits Work

The coordination of benefits process follows a clear sequence. Understanding this sequence helps you predict how your claims will be handled.

Step One — Determine the Primary Plan

The primary insurance plan pays first. It processes your claim as if it were your only coverage. The primary plan applies its normal rules, including deductibles, copayments, and coinsurance, and pays its share of the bill.

Step Two — Send the Remaining Balance to the Secondary Plan

After the primary plan pays, any remaining balance goes to the secondary insurance plan. The secondary plan then reviews the claim and pays according to its own coverage rules. It only considers the amount left after the primary plan has processed its portion.

Step Three — You Pay Any Remaining Balance

If both plans together do not cover the full cost, you are responsible for the remaining amount. However, in many cases, having two plans significantly reduces or even eliminates your out-of-pocket expenses.

Here is a simplified example to illustrate the process:

| Step | Action | Amount |

|---|---|---|

| Medical bill total | Doctor visit charge | 500 USD |

| Primary plan pays | Covers 80% after deductible met | 400 USD |

| Remaining balance | Sent to secondary plan | 100 USD |

| Secondary plan pays | Covers remaining eligible amount | 80 USD |

| Your out-of-pocket cost | What neither plan covered | 20 USD |

Without dual coverage, your share would have been 100 USD. Coordination of benefits reduced it to 20 USD. That is the practical value of understanding how COB works.

How Insurers Decide Which Plan Is Primary

Determining the primary plan is the most critical part of the coordination of benefits process. Insurers follow a standard set of rules established by the National Association of Insurance Commissioners. These rules apply in a specific order.

The Subscriber Rule

If one plan covers you as the primary policyholder (the subscriber) and the other covers you as a dependent, the plan where you are the subscriber pays first. For example, your employer plan where you are the named employee is primary over your spouse’s plan where you are listed as a dependent.

The Birthday Rule for Children

When a child is covered under both parents’ plans, the birthday rule applies. The parent whose birthday falls earlier in the calendar year has the primary plan. This rule uses month and day only, not the year of birth. If one parent’s birthday is March 15 and the other’s is September 22, the March 15 parent’s plan is primary for the child.

The Active vs Inactive Employment Rule

If you have coverage from a current employer and coverage from a former employer (such as retiree benefits or COBRA), the active employer plan is primary. The logic is that current employment coverage takes precedence over legacy coverage.

The Longer Coverage Rule

When none of the above rules resolve the question, the plan that has covered the person longest is typically designated as primary. This serves as a tiebreaker when other determination methods produce no clear answer.

Common Situations Where Coordination of Benefits Applies

Coordination of benefits is not a rare scenario. Several common life situations trigger dual coverage and activate the COB process.

Married Couples With Separate Employer Plans

This is the most frequent COB situation. Both spouses carry their own employer-sponsored health plans and list each other as dependents. Each spouse’s own employer plan is their primary coverage. The other spouse’s plan serves as secondary.

Children Covered Under Both Parents

Children often appear on both parents’ insurance plans. The birthday rule determines which parent’s plan is primary. In cases of divorce, a court order may specify which parent’s plan pays first, overriding the standard rules.

Medicare and Employer Coverage

Individuals aged 65 and older who still work often have both Medicare and an employer plan. If the employer has 20 or more employees, the employer plan is typically primary and Medicare is secondary. For smaller employers, Medicare usually pays first.

Workers With Two Jobs

People who hold two jobs with benefits may be enrolled in two separate employer-sponsored plans. The plan from the job they have held the longest is usually primary, though specific plan terms may vary.

What Coordination of Benefits Means for Your Medical Bills

Understanding coordination of benefits directly impacts how much you pay for healthcare. When COB works correctly, dual coverage can reduce your costs significantly.

However, dual coverage does not mean free healthcare. Your combined benefits from both plans will never exceed 100% of the total allowable medical charges. COB rules specifically prevent overpayment beyond the actual cost of the service.

You should also know that carrying two plans means paying two sets of premiums. Before maintaining dual coverage, calculate whether the premium costs outweigh the savings on medical bills. For families with frequent healthcare needs, dual coverage often provides substantial net savings. For healthy individuals with minimal claims, the extra premium may not be worthwhile.

Always inform both insurance companies that you have dual coverage. Failing to disclose a second plan can delay claims processing and create billing complications. Most insurers ask about other coverage during enrolment and periodically verify your COB status.

Tips to Make Coordination of Benefits Work Smoothly

Managing dual coverage requires a small amount of effort that pays off in fewer billing headaches.

Keep both insurance cards accessible and present them at every provider visit. Give your healthcare provider the primary plan information first, followed by the secondary plan details. This ensures claims are submitted in the correct order from the start.

Review your explanation of benefits statements from both insurers after each claim. Confirm that the primary plan processed the claim first and that the secondary plan applied its coverage to the correct remaining balance. Errors in processing order are the most common COB issue and are usually easy to resolve with a phone call.

If you experience a life event such as marriage, divorce, job change, or turning 65, update both insurers immediately. These events can change which plan is primary and trigger a reassessment of your coordination of benefits arrangement.

FAQs

Coordination of benefits is the process insurers use to determine payment order when you have two or more health plans. It prevents overpayment and ensures your claims are processed correctly.

Insurers follow standard rules including the subscriber rule, birthday rule for children, and active employment rule. The primary plan is the one that pays your claim first.

In some cases, yes. However, combined payments from both plans cannot exceed 100% of the total allowable charge. Your actual savings depend on each plan’s specific coverage terms.

No. The birthday rule only applies to dependent children covered under both parents’ plans. For spouses, each person’s own employer plan is primary and the partner’s plan is secondary.

Yes. You must inform both insurers about your dual coverage. Failing to disclose a second plan can delay claims and create billing disputes that are difficult to resolve later.